Credit Scorecard

A credit decision,

A credit decision,

reasoned end to end

in one surface.

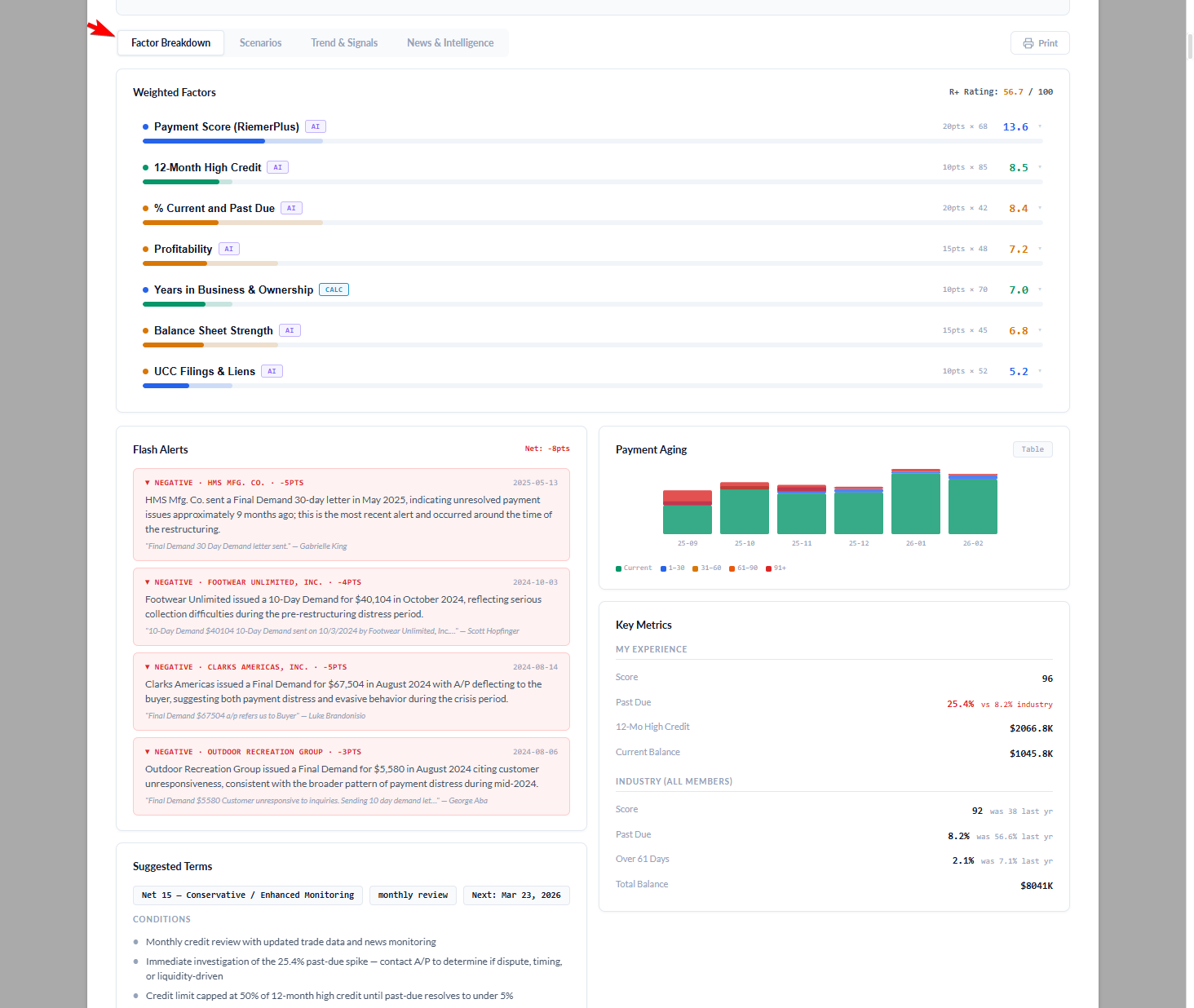

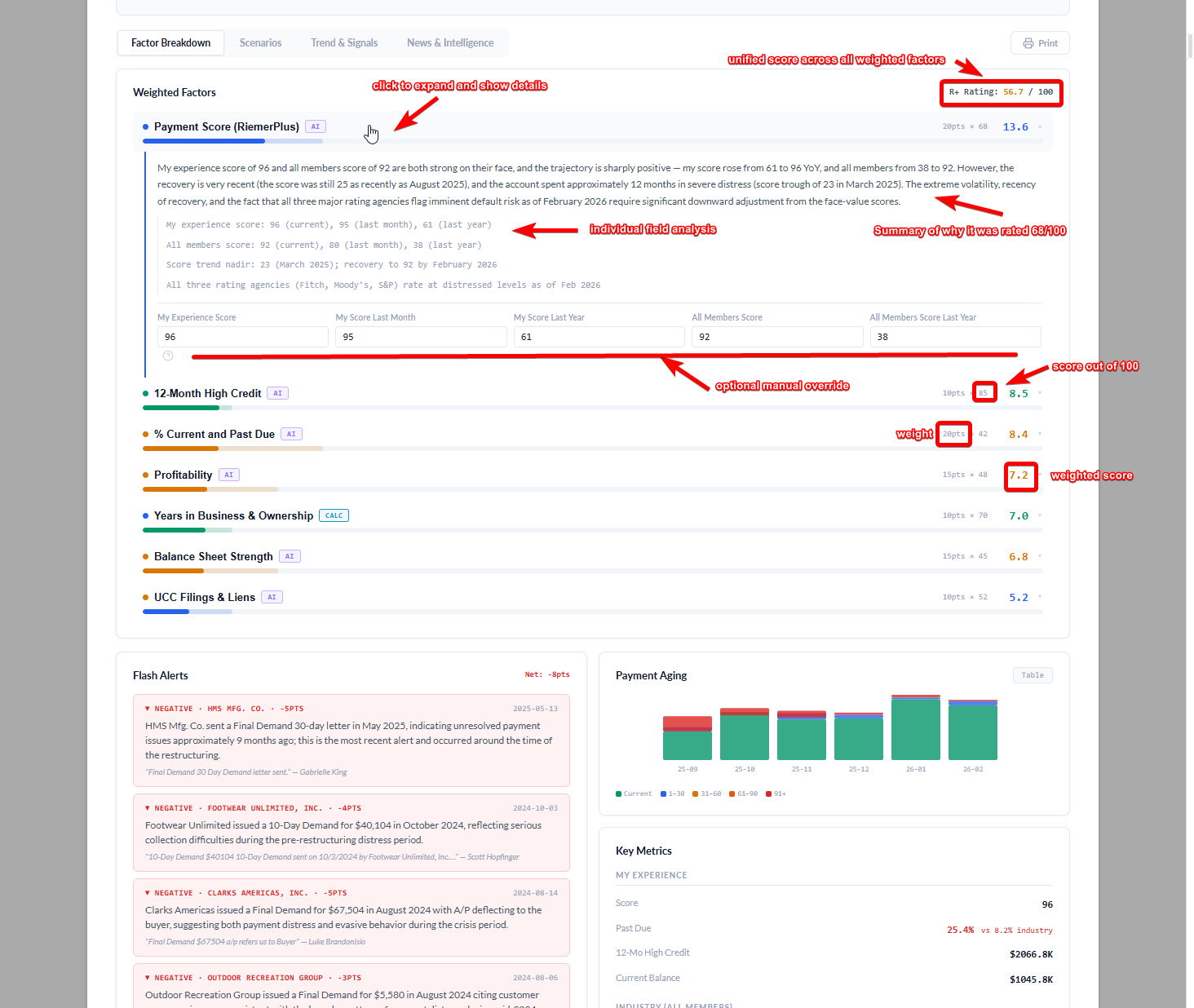

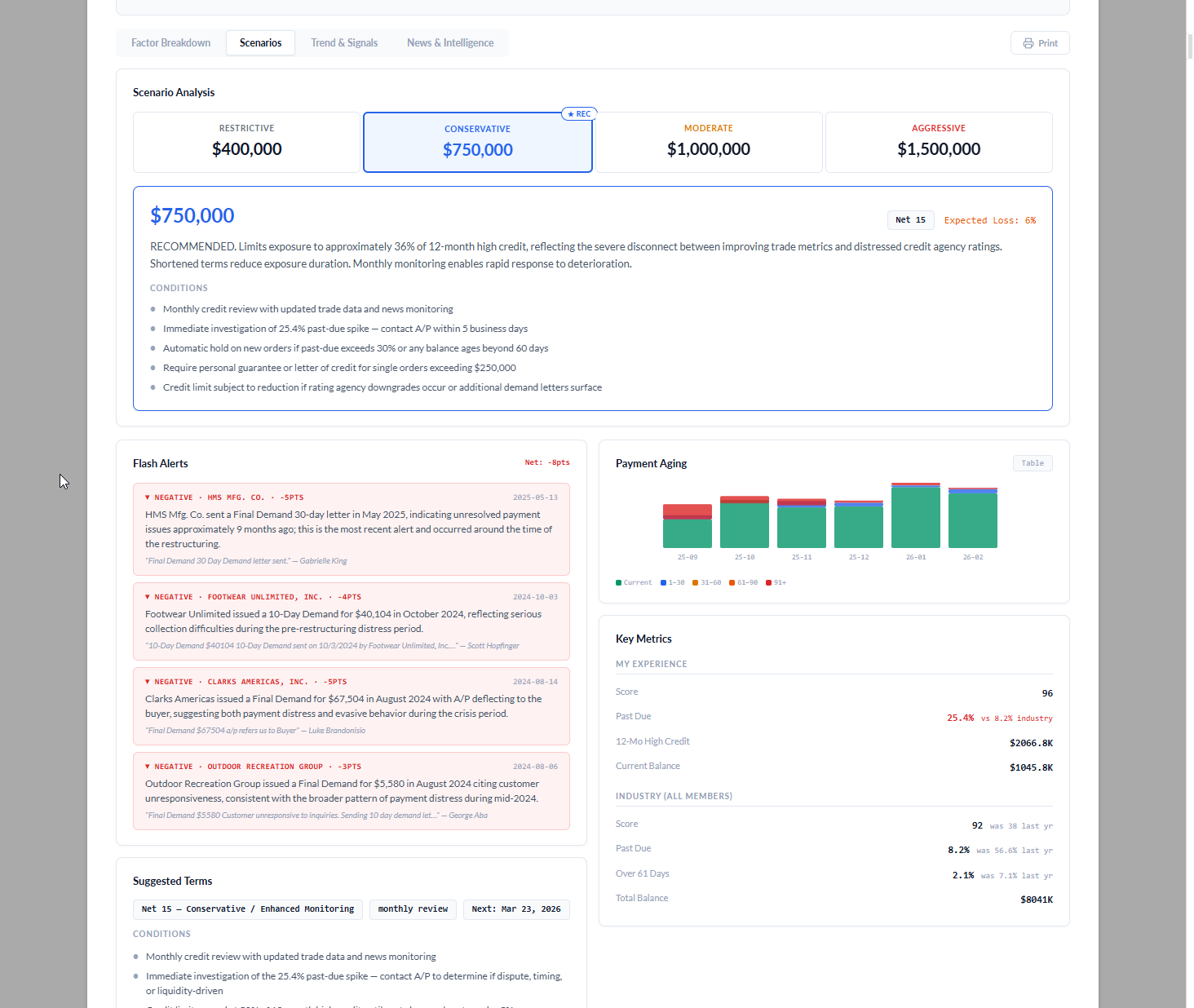

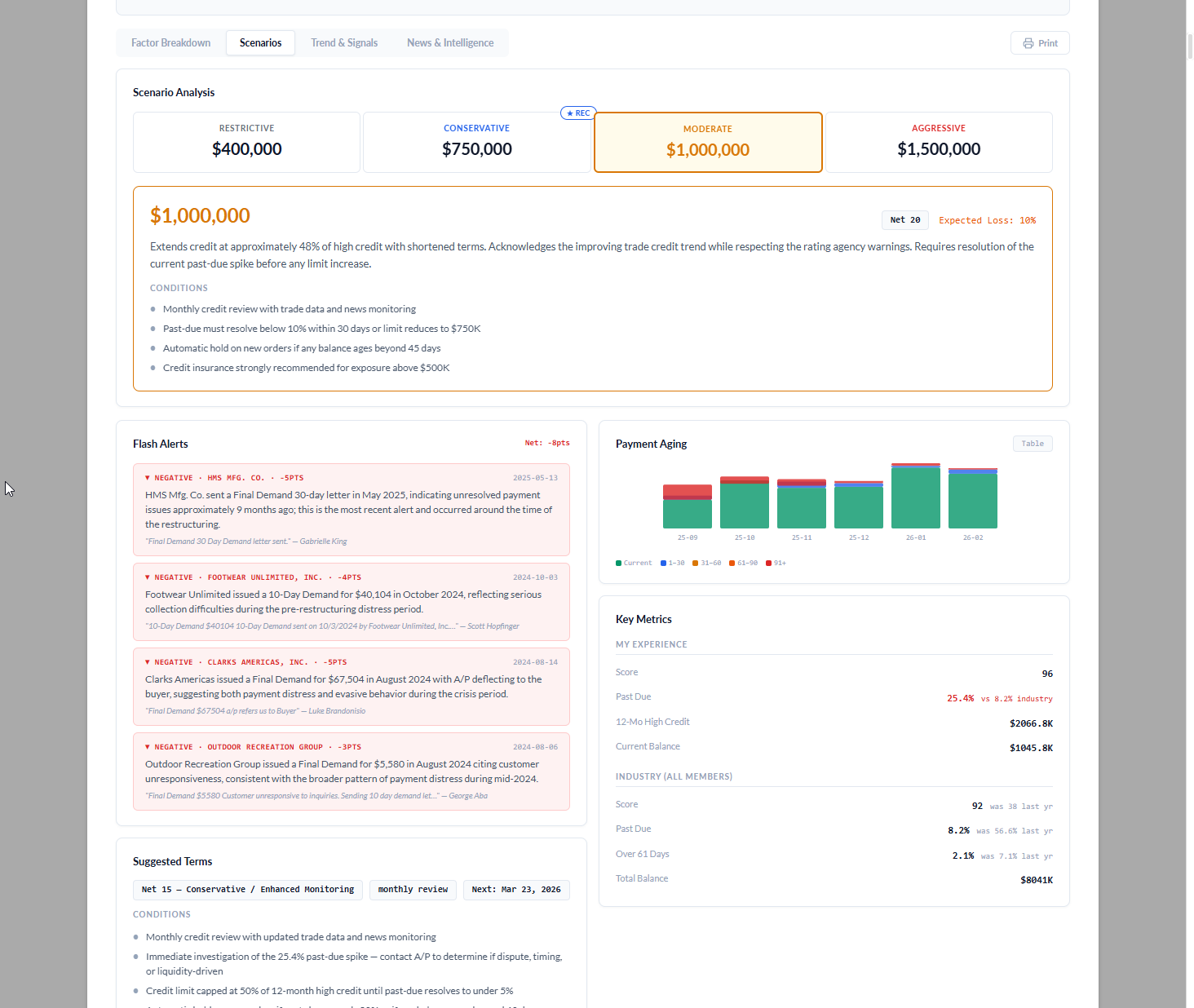

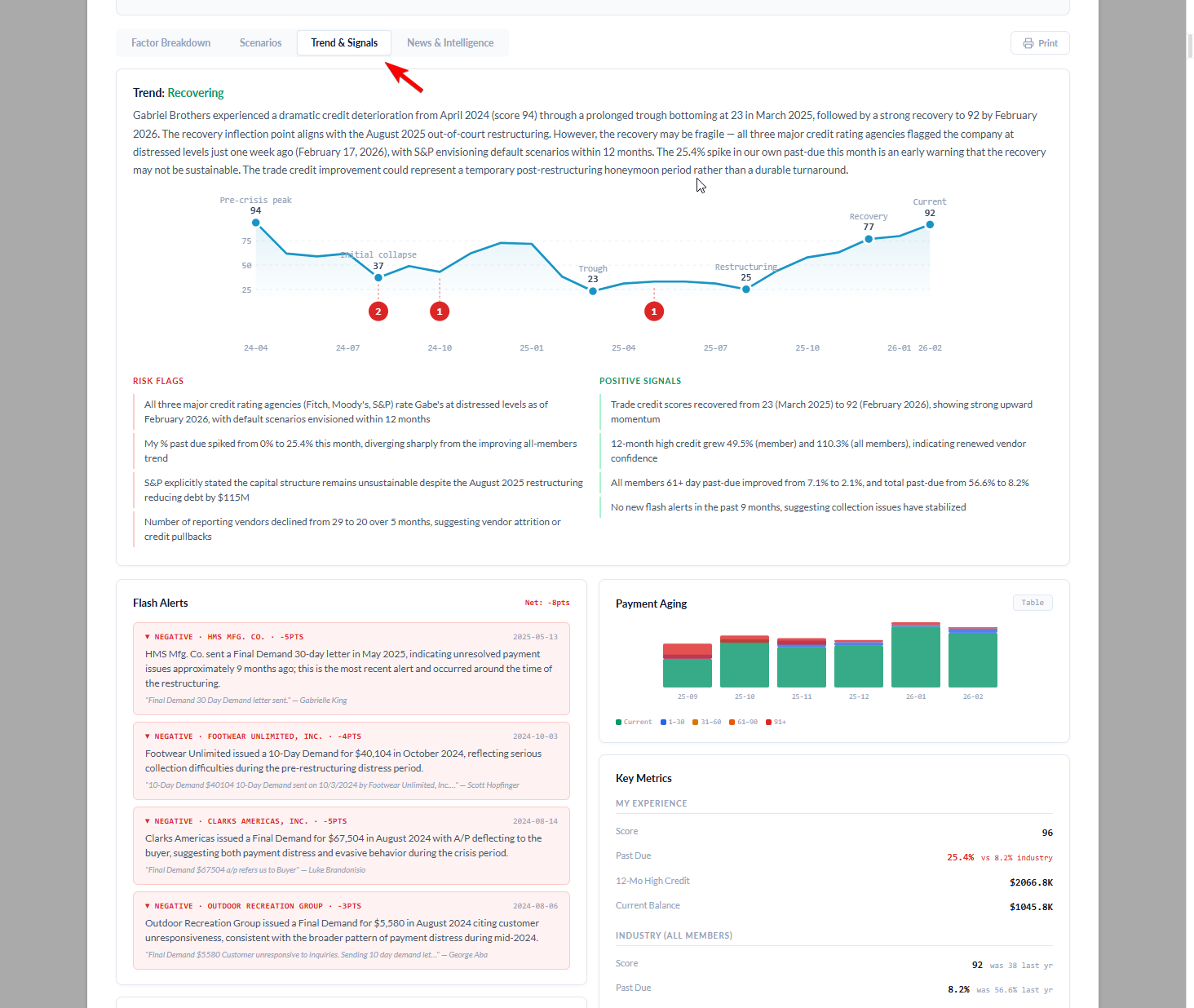

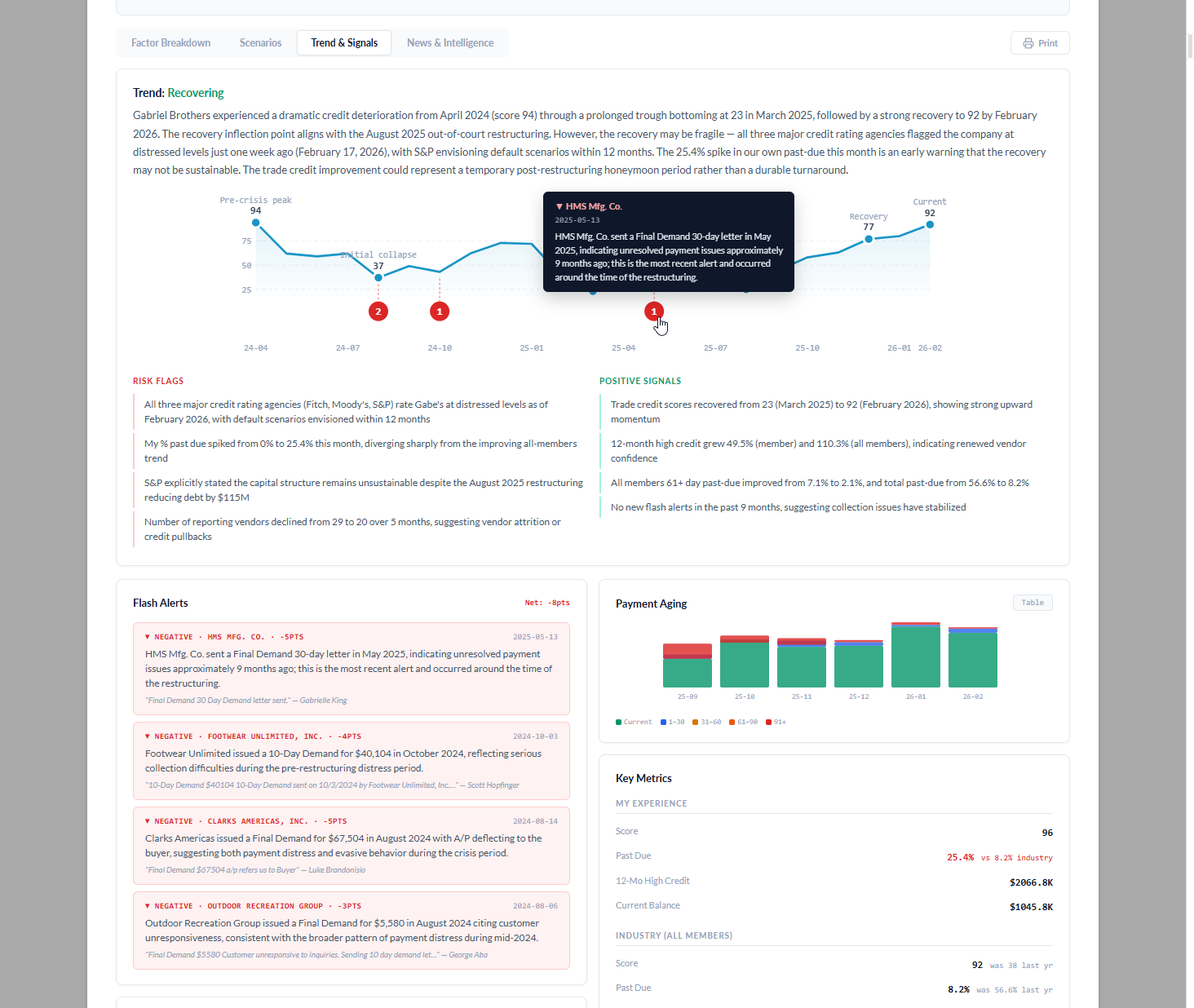

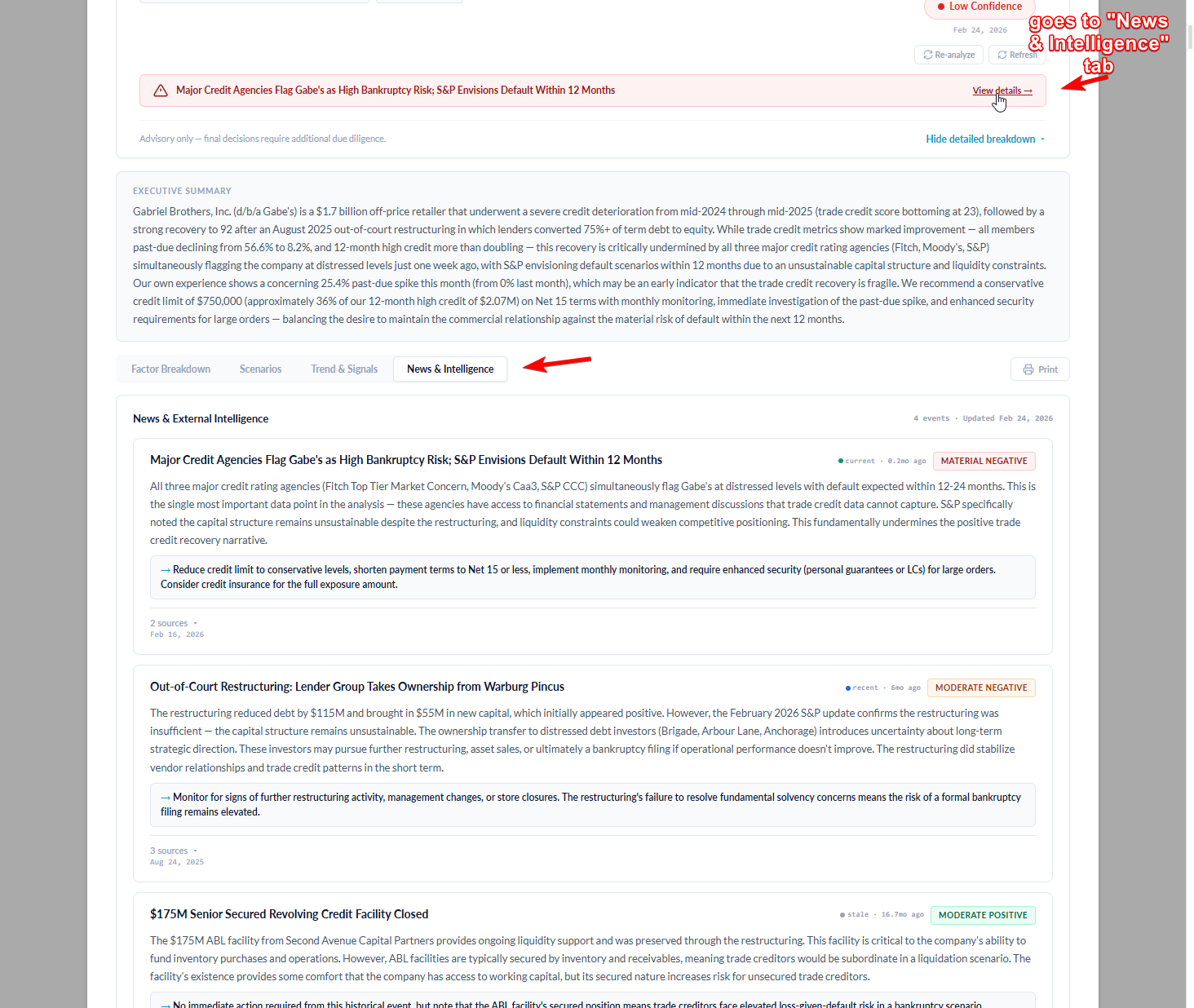

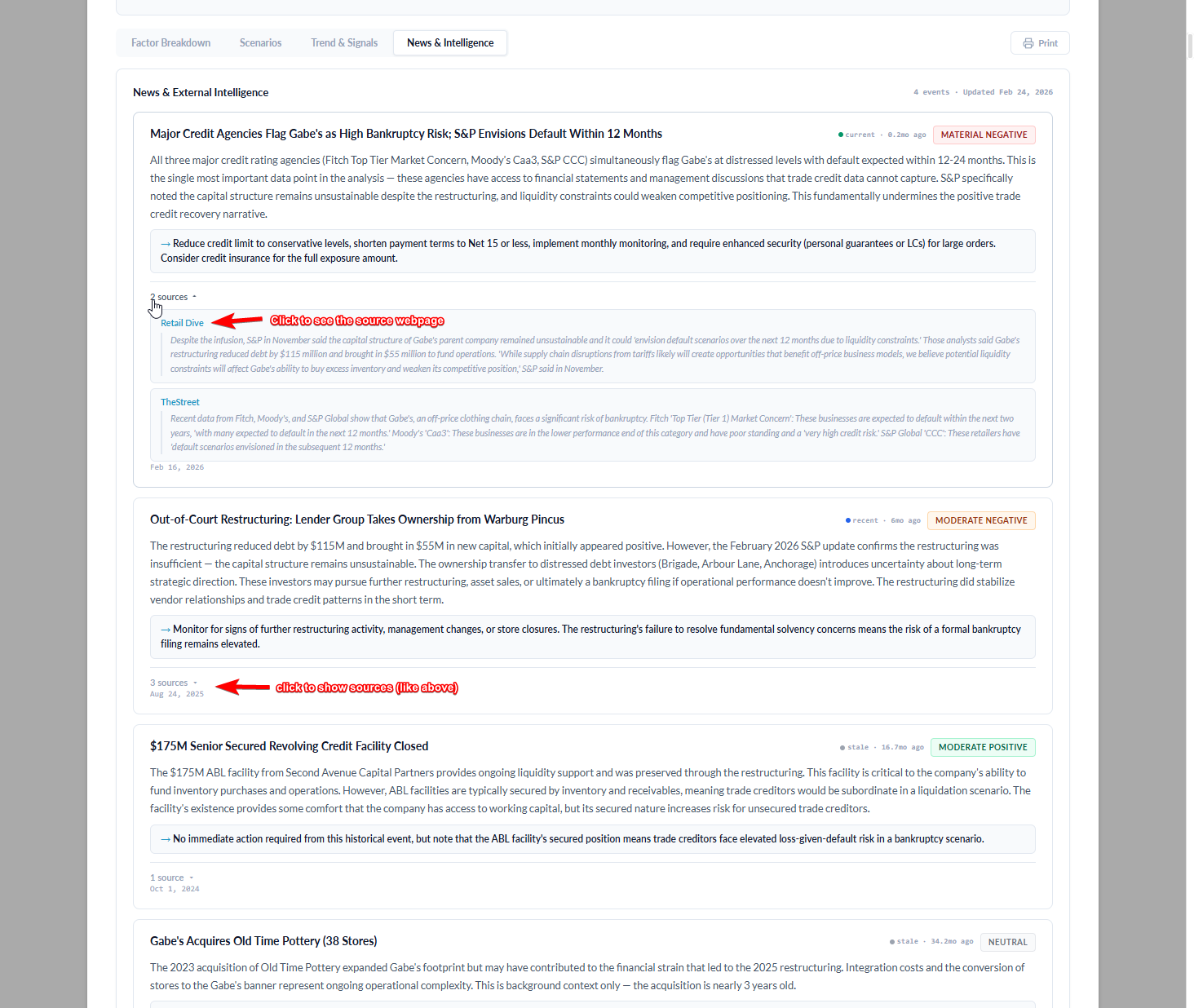

We built an AI-powered credit risk scorecard that fuses trade-credit signals, rating-agency intelligence, and real-time news into a single underwriting view — so a credit analyst can see, understand, and defend a limit recommendation in under a minute.

Client

Commercial credit team

(confidential)

(confidential)

Domain

B2B trade credit

underwriting

underwriting

Built on

Alera — agents,

flows & web UI

flows & web UI

Timeline

Weeks,

not quarters

not quarters